Palomar Holdings (PLMR): Assessing Valuation Following Crop Insurance Expansion and Strategic Acquisitions

: Assessing Valuation Following Crop Insurance Expansion and Strategic Acquisitions")

Palomar Holdings (PLMR) has been turning heads lately with a series of bold moves designed to strengthen its business and reward investors. Most recently, the company signaled its intentions by expanding into the crop insurance segment and closing several strategic acquisitions aimed at boosting scale and diversification. Backed by a healthy capital base, Palomar is also buying back shares, demonstrating management’s confidence in the business and a commitment to delivering value to shareholders.

These actions come at a time when Palomar’s stock price has shown a mix of momentum and volatility. Shares are up over 21% in the past year, building on a steady multi-year performance, although there has been a dip of 28% in the past three months. These swings make sense given the company’s ambitious expansion strategy, ongoing share repurchases, and the natural risks of growing in specialized insurance markets.

The key question now is whether Palomar’s recent moves have created a genuine buying opportunity or if current prices already reflect expectations for continued growth. Are investors looking at value, or is potential future upside already built in?

Most Popular Narrative: 29.9% Undervalued

The widely followed narrative sees Palomar Holdings as significantly undervalued, projecting material upside based on current and future growth assumptions.

Ongoing investment in proprietary technology, data analytics, and advanced underwriting disciplines is improving risk assessment and pricing accuracy. This is already reflected in strong combined ratios and low loss ratios, which should continue to enhance underwriting profitability and expand net margins over time.

Want to know what could push Palomar’s shares even higher? The narrative hints at aggressive growth in both revenue and profits, along with ambitious targets for future pricing. Which key numbers lie behind these bold expectations? See how the forecasted expansion and margin assumptions drive this valuation narrative.

Result: Fair Value of $165.33 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, rapid shifts in competition or a surge in natural disasters could undermine projections and challenge Palomar’s path to sustained growth.

Find out about the key risks to this Palomar Holdings narrative.

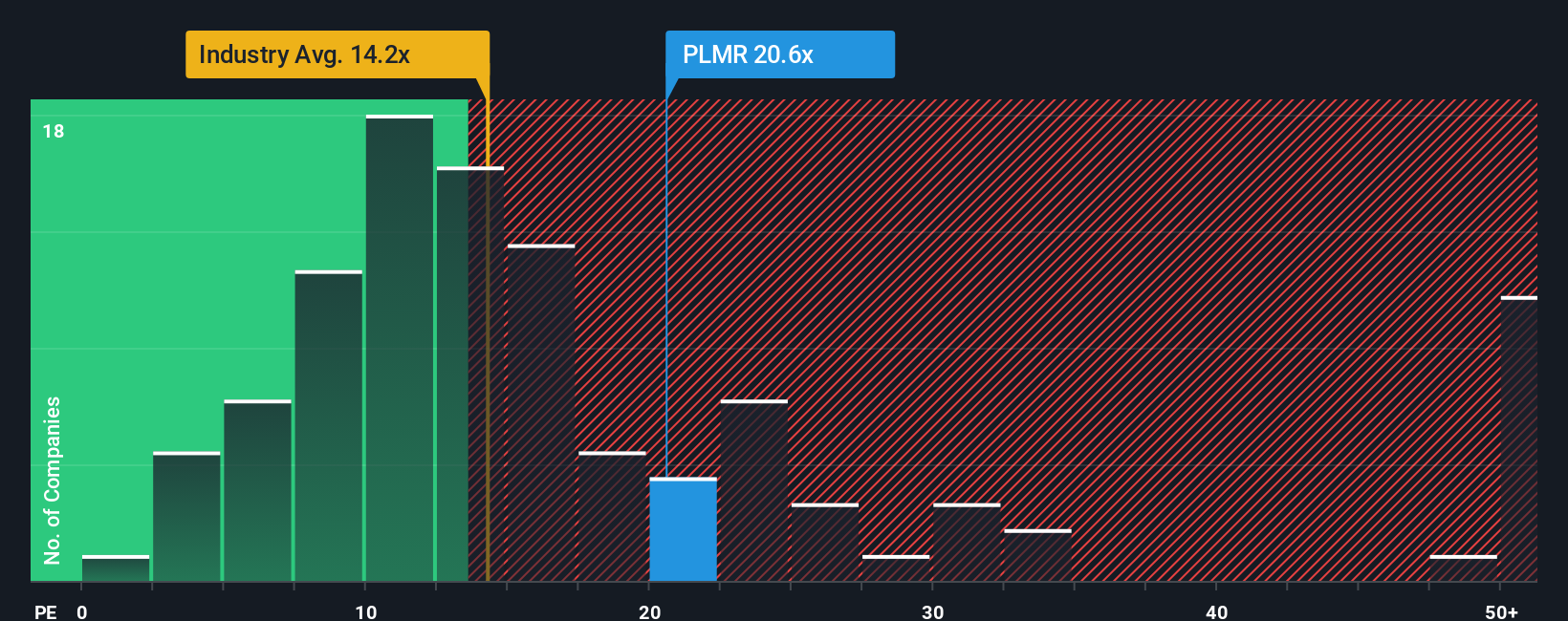

Another View: What Do Traditional Ratios Say?

While our first look found Palomar Holdings undervalued based on future growth and analyst targets, a fresh perspective paints a different picture. Using a common industry valuation ratio, Palomar actually appears more expensive than its insurance peers. This raises the question: are expectations already high, or is the market missing something?

See what the numbers say about this price — find out in our valuation breakdown.

Stay updated when valuation signals shift by adding Palomar Holdings to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own Palomar Holdings Narrative

If our analysis does not match your perspective, or you value hands-on research, there’s always the option to quickly build your own view in just a few minutes. Do it your way.

A great starting point for your Palomar Holdings research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Opportunities?

Don’t limit yourself to a single strategy because smart investors are constantly building watchlists across exciting sectors. Take advantage of powerful tools that make it easy to spot your next winner before the crowd catches on.

- Unlock the potential of cash flow bargains by heading straight to undervalued stocks based on cash flows and explore companies the market hasn’t priced right yet.

- Discover opportunities in healthcare breakthroughs by browsing healthcare AI stocks, where cutting-edge AI meets medical innovation for strong growth potential.

- Boost your portfolio’s income with companies offering yields above 3% using dividend stocks with yields > 3% so you won’t miss reliable payouts while others settle for less.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

link